6/23-27/25 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Week 6/23-27/25

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

Global Weekly Movements

U.S. Equities

S&P 500 Index: 6,173.07 (3.41%)

The SPX blossomed on the week but Energy held the reins back, losing 4.14% over 5 days. The deescalation of geopolitical tensions and inflationary data calmed down the market regarding potential supply chain issues and oil shortages. Communication services, consumer discretionary, and technology sectors led the charge, all increasing by roughly 4%. Leaders in the charge were: META, NFLX, WBD, GOOGL, all respectively rising by 7+%.

Dow Jones Industrial Average: 43,819.27 (3.89%)

Russell 3000 Index: 3,508.54 (3.41%)

NASDAQ Composite: 20,273.46 (4.36%)

Big Movers of the Week

Nike (NKE): 72.04 (20.49%)

Nike jumped 15.2% despite an 86% drop in Q4 profit and 10% revenue decline for FY2025. Management signaled the downturn has likely bottomed, with headwinds expected to ease. Investors are betting on a turnaround, even as CEO Elliott Hill called results “not where we want them to be.” CFO highlighted confidence in “Win Now” actions amid macro uncertainty.

Carnival Corp (CCL): 27.26 (14.68%)

JetBlue’s travel arm, Paisley, LLC, added four major cruise lines: Holland America (CCL), Cunard, Virgin Voyages, and Oceania to its portfolio. The move enhances Paisley's personalized, loyalty-integrated travel services and strengthens JetBlue Vacations’ cruise inventory, especially in luxury and adult-only segments. This signals JetBlue’s deeper push into tech-enabled travel bundling and cross-platform customer retention.

Coinbase (COIN): 353.43 (14.61%)

Coinbase surged 43% in June, leading the S&P 500 since joining the index and marking its best month since November. The rally pushed shares to $382, before settling at $353, still near record highs. Optimism around the GENIUS Act boosted sentiment, shifting focus from trading fees to stablecoin-related income, especially via USDC yield. Analysts see Coinbase as a proxy for Circle’s growth, without the valuation premium. Still, trading volumes remain muted, raising questions about the sustainability of momentum.

Equinix (EQIX): 785.11 (-11.07%)

Equinix dropped nearly 16% this week after management projected 5–9% annual AFFO growth through 2029, well below investor expectations. The slowdown is due to surging AI-driven capex needs, as the company expands data center capacity to meet future demand. Analysts reacted swiftly, with downgrades from Raymond James and BMO.

Chinese Equities - Shanghai Composite (SHCOMP): 3,424.23 (2.23%)

Hong Kong Equities - Hang Seng Index (HSI): 24,284.15 (4.07%)

Japanese Equities- Nikkei 2225 (NI225): 40,150.79 (4.94%)

European Equities

UK Index (UKX): 8,798.91 (0.28%)

German Index (DAX): 24,033.22 (3.40%)

Commodities

Gold Futures: 3,286.10 (-2.73%)

Crude Oil Futures: 65.07 (-13.57%)

U.S. Monetary & Fiscal Policy:

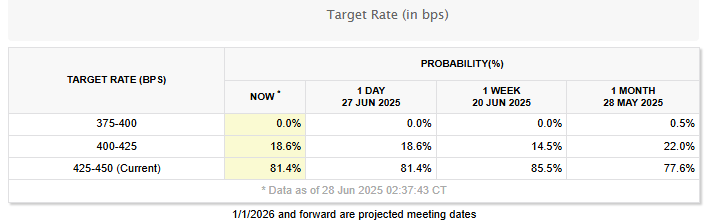

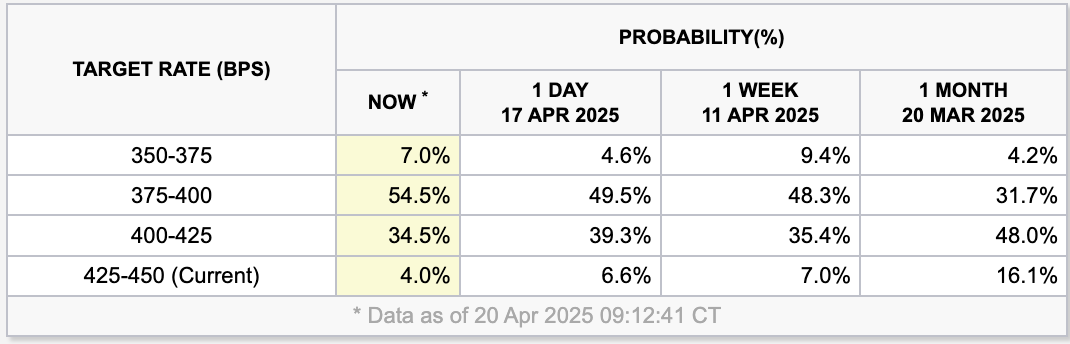

July 30th FOMC Meeting: Markets have walked back aggressive rate cut expectations as inflation remains sticky and consumer data weakens. Back on April 20, traders priced in a 55% chance of a 50 bps cut and 35% odds of a 25 bps cut at the July 30 FOMC meeting, reflecting hopes for swift Fed easing. Now, with core PCE at 2.7% and consumption softening, markets assign 0% probability to a 50 bps cut, and just 18.6% confidence in a 25 bps cut, per Fed funds futures. This shift underscores the Fed’s cautious tone and growing concern over tariff-driven inflation later this summer.

Global Macroeconomic News:

Consumer Sentiment: U.S. consumer sentiment improved for the first time in six months, with the University of Michigan index rising to 60.7 in June from 52.2 in May. The gain was driven by broad-based improvements in views on personal finances and business conditions, both up more than 20%. The current conditions index rose sharply, while expectations dipped slightly from the preliminary reading but remained significantly higher than in May. Inflation expectations fell notably, with year-ahead expectations dropping to 5.0% from 6.6% and long-run expectations edging down to 4.0%.

GDP (Second Revision): The U.S. economy contracted by 0.5% in Q1 2025, a sharper drop than earlier estimates, marking the first decline in three years. The pullback was driven by a surge in pre-tariff imports, which dragged on headline GDP. However, underlying demand (real final sales to private domestic purchasers) still grew 1.9%, albeit slower than Q4’s 2.9%. Consumer spending weakened sharply to 0.5%, the slowest pace since the pandemic. Economists expect a rebound in Q2, with growth projected at 3% as the tariff-related distortions fade.

PCE & Core PCE: Core PCE, the Fed’s preferred inflation gauge, rose 2.7% YoY in May, above the expected 2.6%, while headline PCE held at 2.3%. Monthly price growth remained modest, but consumer spending fell 0.1% and personal income dropped 0.4%, both missing expectations. The data shows sticky services inflation and softening consumer demand. Markets are still pricing in a cautious Fed, with July rate cut hopes alive but fading. The report reinforces a gradual cooling narrative ahead of expected tariff impacts later this summer.

Sources: Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, New York Times, Bloomberg, Wall St Journal, Washington Post, US Department of the Treasury, Zacks

Have a great week investing!

Sincerely,

Aremorph

Comments

Post a Comment