5/26/25 - 5/30/25 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Week 5/26-30/25

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

Global Weekly Movements

U.S. Equities

S&P 500 Index: 5,911.69 (2.24%)

This week, all sectors the the SPX were positive, with real estate leading the charge at 2.68%, followed by financials at 1.82%. Energy was the only sector negative for the week. Markets have recovered over the past months to previous end of year highs, despite all the volatility introduced in the beginning of the year, investor optimism has returned.

Dow Jones Industrial Average: 42,270.07 (1.79%)

Russell 3000 Index: 3,360.01 (2.09%)

NASDAQ Composite: 19,113.77 (2.64%)

Big Movers of the Week

HP (HPQ): 24.90 (-12.63%)

HP reported a 3% year-over-year increase in revenue to $13.2 billion, slightly beating expectations, but its adjusted net income dropped sharply to $678 million, missing analyst forecasts. The company cited strong commercial performance in personal systems, though profitability was pressured, and it cut full-year earnings guidance due to tariff concerns. With a stagnant PC market and potential headwinds from international trade, investor sentiment around HP stock remains cautious.

Ulta Beauty (ULTA): 471.46 (17.00%)

Ulta Beauty shares jumped after it reported strong quarterly results and raised its outlook. The company saw solid growth in both store and online sales, driven by better performance with teen and value-focused customers and features that improved digital engagement. Analysts highlighted Ulta’s improving momentum and believe its turnaround strategy is setting the stage for steady growth and stronger profits.

Intuit (INTU): 753.47 (13.12%)

Intuit has recently attracted attention as its stock outperformed the broader market and software sector over the past month. The company, known for products like TurboTax and QuickBooks, is benefiting from positive momentum and rising investor interest. According to Zacks, upward revisions in earnings estimates are a key driver of future stock gains, and Intuit’s improving outlook suggests potential for continued price strength in the near term.

Chinese Equities - Shanghai Composite (SHCOMP): 3,347.49 (0.03%)

Hong Kong Equities - Hang Seng Index (HSI): 23,289.77 (-0.92%)

Japanese Equities- Nikkei 2225 (NI225): 37,965.10 (2.03%)

European Equities

UK Index (UKX): 8,772.38 (0.38%)

German Index (DAX): 23,997.48 (-0.05%)

Commodities

Gold Futures: 3,313.10 (-0.50%)

Crude Oil Futures: 60.79 (0.02%)

U.S. Monetary & Fiscal Policy:

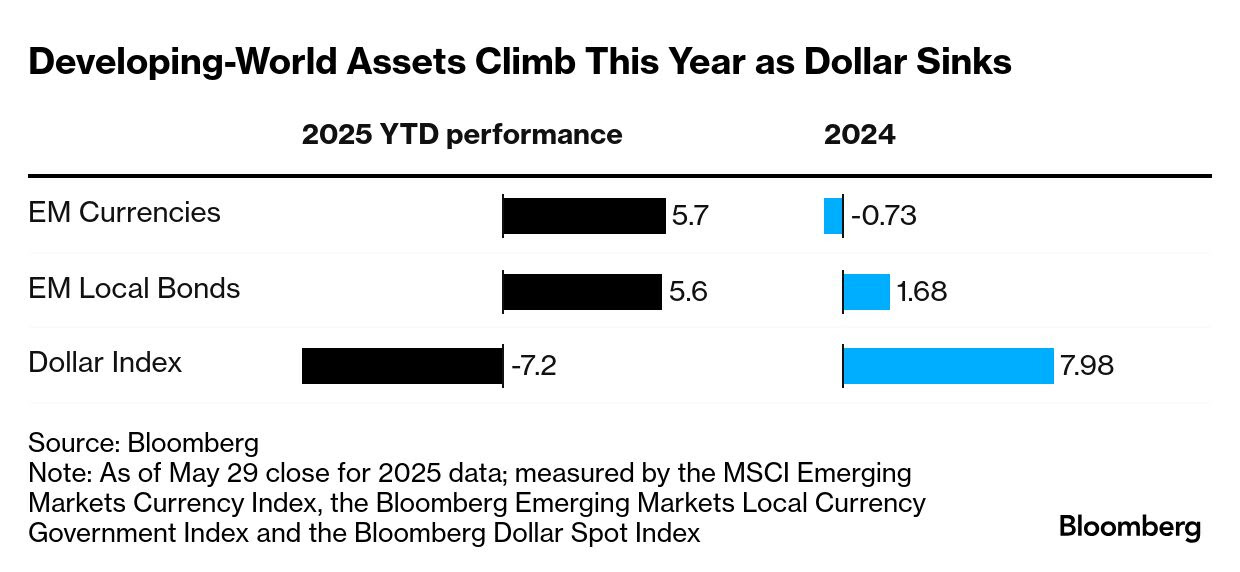

USD Performance: Against emerging markets, the USD continues to decrease in value and strength. Increases in volatility shift investor demand away from the dollar, coupled with the projection of continued rate cuts, the investment opportunities and attractiveness diminish.

Dimon Declares: Jamie Dimon warned a U.S. bond market disruption is inevitable due to excessive government spending and Fed easing, though the timing is unclear. He urged reforms to debt policy and banking regulations to prevent a crisis. Treasury losses in May reflect growing investor unease amid Trump’s policy shifts and deficit concerns. Dimon expects the Fed will eventually need to intervene. While JPMorgan would manage fine, he said such a crisis might finally spur necessary reforms.

Global Macroeconomic News:

PCE & Core PCE: In April 2025, U.S. inflation eased more than expected, with the Fed’s preferred gauge—the personal consumption expenditures (PCE) index—rising just 0.1% monthly and 2.1% annually, the lowest in 2025 so far. Core PCE inflation, excluding food and energy, also rose just 0.1% on the month and 2.5% annually, slightly below estimates. Consumer spending slowed sharply to a 0.2% monthly gain, while the savings rate jumped to 4.9%, suggesting growing caution among households. Personal income, however, rose a strong 0.8%, beating expectations. Despite subdued inflation, markets remained largely unmoved, as uncertainty looms over President Trump’s tariffs and their potential to drive inflation higher later this year.

Consumer Sentiment: Consumer sentiment improved slightly in late May, with the UMich index rising to 52.2 from 50.8 earlier in the month, matching April’s level but still 25% below a year ago. The uptick was driven by a pause in some U.S. tariffs on Chinese goods, which eased fears about economic damage. Current economic conditions were viewed more positively, and short- and long-term inflation expectations dropped to 6.5% and 4.25%, respectively, from earlier readings.

Japanese Creditor Position: Japan lost its position as the world’s largest creditor nation for the first time in 34 years, with Germany overtaking it in 2024 despite Japan’s record-high net external assets of ¥533.05 trillion. Germany’s assets reached ¥569.7 trillion, boosted by a strong current account surplus and a favorable euro-yen exchange rate. Japan’s long-held top status was driven by decades of surpluses and overseas investments, but recent trends show stronger real demand and asset accumulation in Germany and China. Japanese companies continue to expand direct investments abroad, particularly in the US and UK, though such investments are harder to reverse compared to securities.

Sources: Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, New York Times, Bloomberg, Wall St Journal, Washington Post, US Department of the Treasury, Zacks

Have a great week investing!

Sincerely,

Aremorph

Comments

Post a Comment