4/21/25 - 4/25/25 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Week 4/21/25 - 4/255/25

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

Global Weekly Movements

U.S. Equities

S&P 500 Index: 5,525.21 (5.59%)

All sectors of the SPX are up this week, except for consumer stables (XLP), down 1.26%. Technology led the charge at 8.09% growth, riding the tail winds of positive news regarding fiscal policy moving forward. Investor sentiment in the future of America remains strong as consumer discretionary stocks rise just under 7%. Despite this recovery, caution still remains for how long the initial slide in equities will last.

Dow Jones Industrial Average: 40,113.50 (3.10%)

Russell 3000 Index: 3,139.45 (5.63%)

NASDAQ Composite: 17,382.94 (8.29%)

Big Movers of the Week

Service Now (NOW): 945.26 (22.42%)

After strong earnings reports and CEO William McDermott emphasizing the growth in AI despite tariff challenges, investors show conscience in the future prospects.

Palantir (PLTR): 112.78 (20.26%)

Following an announcement in partnership with Google, shares of Palatir extend their 4 day winning streak. Planter's dominance in the past year was fueled by investor confidence and as AI technology advances, the future looks bright for PLTR.

Tesla (TSLA): 284.95 (18.06%)

Despite the negative earnings, missing nearly every metric, TSLA stock rises. Investors are hopeful that fiscal headwinds will dampen, allowing manufacturing costs to cease margin compression and expand demand for EV’s.

Netflix (NFLX): 1101.53 (13.21%)

Robust quarterly earnings from Netflix rallied confidence as well as positive outlooks onto the future. Netflix plans to breach the 1 trillion dollar equity value milestone by the end of the decade.

Chinese Equities - Shanghai Composite (SHCOMP): 3,295.06 (0.67%)

Hong Kong Equities - Hang Seng Index (HSI): 21,980.74 (4.34%)

Japanese Equities- Nikkei 2225 (NI225): 35,705.74 (3.33%)

European Equities

UK Index (UKX): 8,415.25 (1.69%)

German Index (DAX): 22,242.45 (3.77%)

Commodities

Gold Futures: 3,330.20 (-1.88%)

Crude Oil Futures: 63.17 (0.21%)

U.S. Monetary & Fiscal Policy:

Impact of Tariffs on China: After aggressive tariffs on China, respective plastic factories which rely strongly on US ethane are facing potential shutdowns as tariffs cause imports economically unviable. This dramatic increase in price expands the spread between demand and supply, causing a shortage that domestic Chinese production is unable to cover. This highlights the impact of US fiscal policy in the world, as a dominant import and export country, as well as holding the global reserve currency.

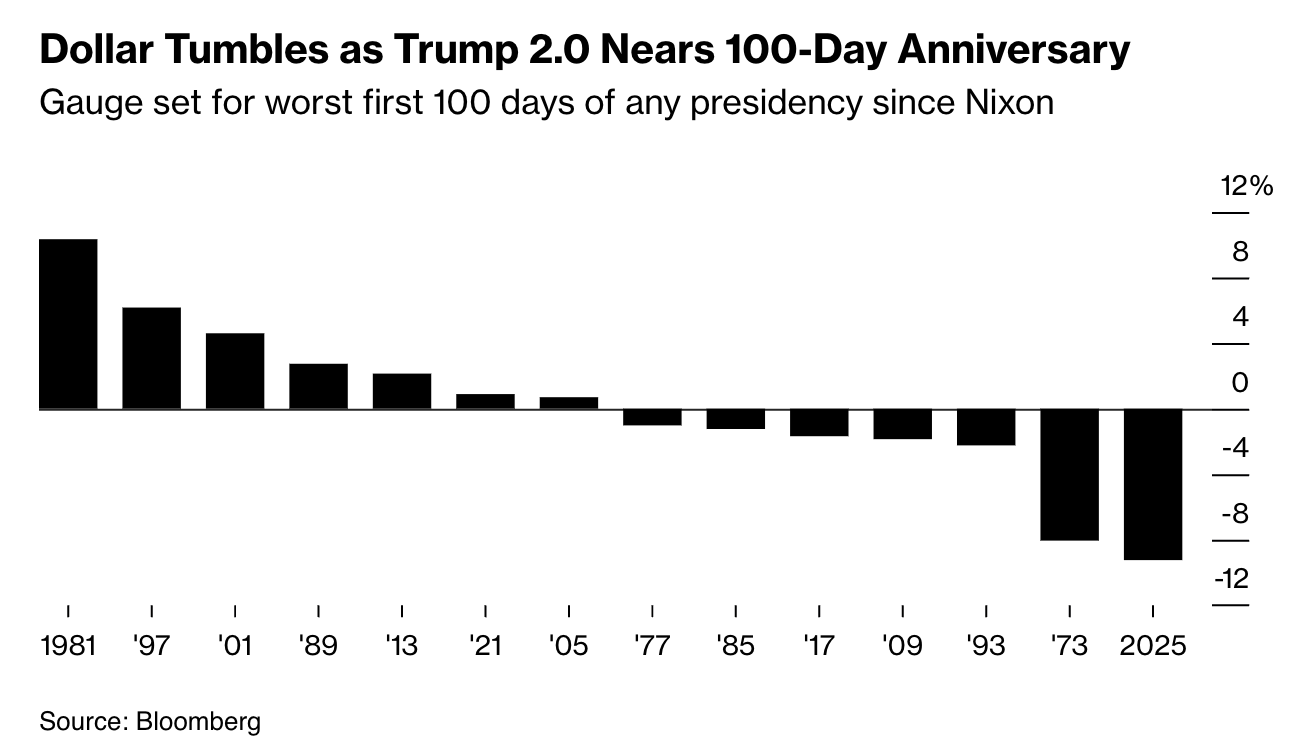

Dollar Weakens: From the highs of 110 in late January, the dollar index (DXY) has fallen to below 100. This is the worst first 100 days under a new presidency since the era of Nixon. Despite the expectations of the dollar to strengthen under tariffs as the reserve currency, the implementations have caused extreme weakness. Investors are placing confidence into foreign assets, boosting foreign currencies against the USD. Trump continues to push Powell for continuation of the easing cycle on interest rates, but if the interest rates were to decrease, the international yield spread would expand, making foreign fixed income investments attractive, and weakening the dollar.

Global Macroeconomic News:

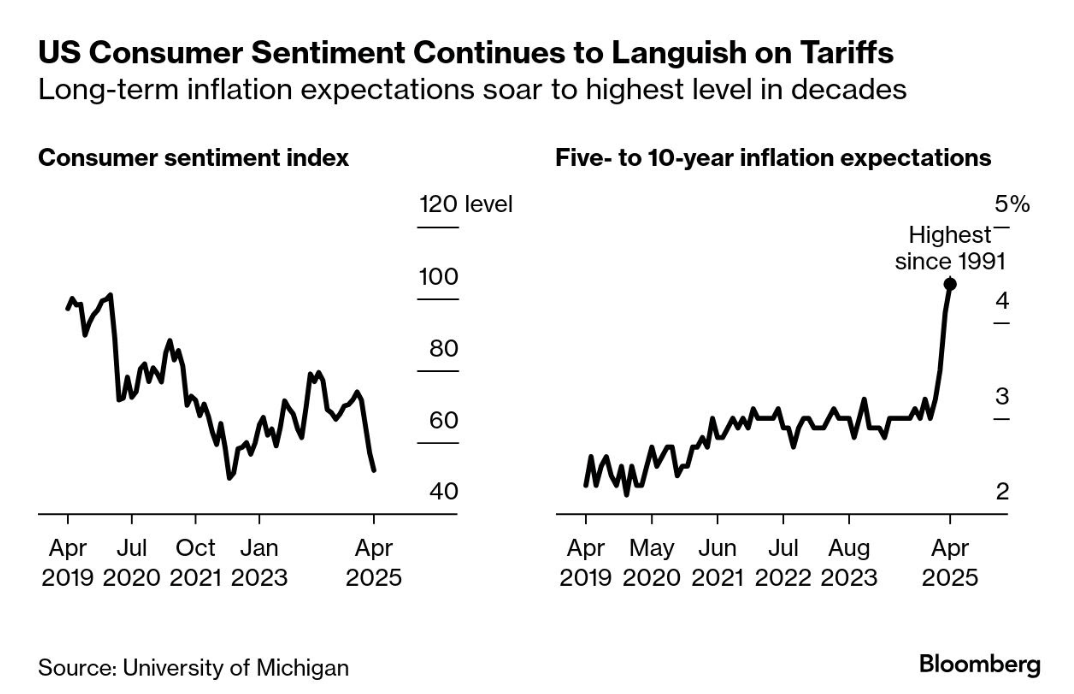

Final Consumer Sentiment + Inflation Outlook: A record fall in US consumer sentiment occured in April. With the index dropping to 52.2, the fourth lowest since 1970, the illustration of fear infiltrating the markets as tariffs grow is evident. Moreover, long-term implantation expectations grow to 4.4%, the highest since 1991. As prospective inflation ticks up, short term demand increases to “beat inflation” but in reality, will increase inflation on top of potentially lagging inflation.

Nomura to Buy Macquire: Nomura agreed to acquire Macquire's US and European public asset management division in an all stock transaction. This deal would expand Normura’s command on a global scale, chartering horizons across the world. This shift aligns closely with the 2030 global growth plan.

Sources: Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, New York Times, Bloomberg, Wall St Journal, Washington Post, US Department of the Treasury

Have a great week investing!

Sincerely,

Aremorph

Comments

Post a Comment