4/14/25 - 4/18/25 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Week 4/14/25 - 4/18/25

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

Global Weekly Movements

U.S. Equities

S&P 500 Index: 5,282.70 (0.52%)

All sectors of the SPX are positive on the week except technology, consumer discretionary, and communication services, reflecting the inflationary sentiment and consumers falling back to more staples. Real Estate saw a large increase with over 5% gains on the week, a combination of factors including interest rates, tariffs, and local demand.

Dow Jones Industrial Average: 39,142.23 (-0.89%)

NASDAQ Composite: 16,286.45 (-0.44%)

Russell 3000 Index: 3,001.15 (0.79%)

Big Movers of the Week

UnitedHealth Group (UNH): 454.11 (-23.60%)

After missing Q1 earnings due to higher-than-expected Medicare costs, raising concerns about the broader insurance sector, shares slide. Jefferies warned that if these issues are widespread, other insurers could also face trouble, though UnitedHealth may have simply set overly aggressive expectations.

Global Payments (GPN): 69.46 (-16.55%)

Despite a large merger with an expected accretive pro-forma EPS. Under the current macroeconomic and geopolitical environment, Jefferies equity research highlights “long-term challenges that are unlikely to find support in the current backdrop.”

Eli Lilly (LLY): 839.96 (16.51%)

Eli Lilly's new oral GLP-1 weight loss drug, orforglipron, showed strong results in a Phase 3 trial, causing its stock to surge. The once-daily pill, which showed significant blood sugar and weight reduction without notable side effects, sets Lilly up to dominate the GLP-1 pill market if future trials succeed. Unlike Pfizer, which recently abandoned its own GLP-1 pill effort, Lilly plans to launch orforglipron globally without supply issues, potentially leaving rivals scrambling to catch up.

Dollar Tree (DLTR): 79.14 (10.32%)

After strong insider buying activity by the CFO, investors are rallied in confidence. Low cost retailers are seeing positive impacts of increased prices, as the expectation of consumers to turn away from discretionary goods increases.

Chinese Equities - Shanghai Composite (SHCOMP): 3,291.41 (0.94%)

Hong Kong Equities - Hang Seng Index (HSI): 21,395.14 (4.07%)

Japanese Equities- Nikkei 2225 (NI225): 34,402.45 (0.16%)

European Equities

UK Index (UKX): 8,275.66 (4.58%)

German Index (DAX): 21,20586 (2.01%)

Commodities

Gold Futures: 3,388.0 (4.65%)

Crude Oil Futures: 63.59 (6.36%)

U.S. Monetary & Fiscal Policy:

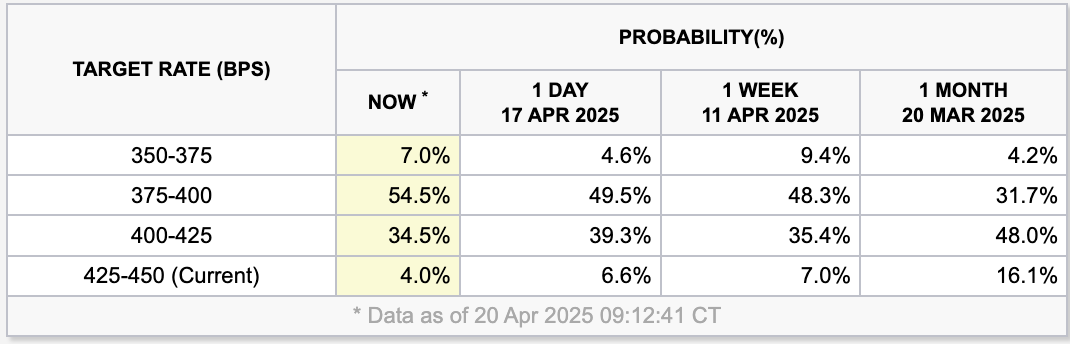

Two Cuts Priced: CME Fedwatch indicates that after the July 30, 2025 FOMC meeting, market sentiment points at the federal funds rate range between 375 - 400 bps. This comes as a relief in market sentiment given the fear of heavily inflationary fiscal policy policies implemented earlier in 2025. This continuation of the easing cycle that began late 2024 will likely have positive implications for both equity markets and debt capital markets. Equity will seem relatively more attractive as fixed income investment yield falls to match the borrowing costs and borrowing will become cheaper, incentivising more borrowing and capital expenditures. This can all have a positive impact on the second mandate of the Fed, regulating the labor market.

Global Macroeconomic News:

Retail Sales: Consumer spending in March was stronger than expected, with retail sales rising 1.4%—the biggest monthly gain since January 2023—despite weak consumer sentiment and fears of looming tariffs. Excluding autos, sales still beat forecasts, and motor vehicle and parts dealers saw a sharp 5.3% jump as consumers rushed to buy ahead of potential price hikes. The strength in spending extended to several categories, including building materials, food services, and hobbies, even as gasoline sales fell. Despite the strong report, markets had a muted reaction, as fears about inflation and recession persist, underscored by consumer sentiment data showing deep concerns.

International Semiconductor Trade: TSM stock has fallen 25% YTD, indicating that the tariffs on semiconductor chips, slowing growth expectations. TSMC beat expectations in Q1, posting $11.1B in profit as U.S. customers rushed to stock up on chips ahead of potential tariffs. But despite the strong quarter, investors are more focused on what 2025 will look like, especially with rising trade tensions and U.S. export restrictions creating uncertainty for key customers like Apple and Nvidia. There’s talk that TSMC may scale back its sales growth forecast, or pull guidance entirely.

ECB Rate Cut: The European Central Bank cut its key interest rate to 2.25% on Thursday, citing growing trade tensions following U.S. tariffs that have sparked fears of a global trade war. ECB President Christine Lagarde warned that uncertainty is weighing on business investment and consumer confidence, while other global institutions, including the IMF and Fed Chair Jerome Powell, have echoed concerns about the economic fallout. The rate cut marks the ECB’s seventh in the past year, contrasting with the Fed’s decision to hold rates steady amid similar concerns. Trump criticized Powell’s approach, but Lagarde defended central bank independence and voiced strong support for her U.S. counterpart.

Sources: Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, New York Times, Bloomberg, Wall St Journal, Washington Post, US Department of the Treasury, GuruFocus

Have a great week investing!

Sincerely,

Aremorph

Comments

Post a Comment