2/24-28/25 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Week 2/24-28/25

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

Continued tariffs and DOGE layoffs from our President and Musk keep the market on edge while the tech sector plummets amidst lower than expected earnings and political turmoil. Changes in the labor market and jobless claims report this week played an impact into how market impact views future FOMC results.

Global Weekly Movements

U.S. Equities

S&P 500 Index: 5954.50 (-1.20%)

Market remained divided with Financials and Real Estate leading at 2.82% and 2.18% while Technology fell at -3.98% respectively. Financials up due to Trump foreign policy and stance on M&A approval, potentially enhancing fee revenue, while real estate creeps up due to positive interest rates. With technology making up around a third of the SPX, the sector drove down amidst Trump tariffs, deepseek reversal, and NVIDIA’s earning report.

Dow Jones Industrial Average: 43840.91 (0.80%)

Russell 3000 Index: 3389.87 (-1.23%)

NASDAQ Composite: 18847.28 (-3.80%)

Big Movers of the Week

Palantir (PLTR): 84.90 (-11.31%)

Palantir stock plummets with news of the Pentagon forming plans to cut US military spending by 8% over the next five years. With roughly half of 2024 revenue coming from US government related contracts, the stock fell a third from its previous all time high.

Tesla (TSLA): 293.04 (-13.24%)

Tesla stock fell around a third in February following concerns over failing low Q4 earnings, European sales, and an increase in EV competition. CEO Musk’s political controversies and DOGE involvement also continue to be worrisome for investors. Following the company's second worst month ever, the company remains optimistic banking on upcoming robotaxi initiatives and a new Texas factory.

Super Micro Computer (SMCI): 41.36 (-23.03%)

SMCI regains NASDAQ listing compliance after filing delayed financial reports. Has predicted increased revenue for fiscal year 2026 after expecting an increase in demand for products to support AI.

Moderna (MRNA): 30.96 (-8.86%)

Sales prediction dropped after forecasts of 17% decline in vaccine business. With the Covid-19 pandemic over, Moderna faces hard times ahead. Analysts polled by S&P Global Market Intelligence also predicted Moderna will not be profitable until 2029.

Chinese Equities - Shanghai Composite (SHCOMP): 3320.90 (-1.58%)

Hong Kong Equities - Hang Seng Index (HSI): 22941.32 (-2.26%)

Japanese Equities- Nikkei 2225 (NI225): 37155.50 (-3.55%)

European Equities

UK Index (UKX): 8809.74 (1.74%)

German Index (DAX): 22551.43 (0.36%)

Commodities

Gold Futures: 2867.30 (-2.93%)

Crude Oil Futures: 69.95 (-0.27%)

U.S. Monetary & Fiscal Policy:

Tariff Retaliation: The EU is preparing retaliatory tariffs on U.S. goods if Trump imposes new steel and aluminum duties, potentially affecting €28B in exports. While trade chief Maros Sefcovic offered a deal on industrial tariffs to prevent escalation, negotiations remain uncertain. The EU aims for a WTO-compliant response, targeting politically sensitive industries like whiskey, motorcycles, and steel. With no exemptions planned, tensions could surpass the 2018 trade conflict, impacting key sectors on both sides. Expect the implementation of these to move a bearish front into the markets.

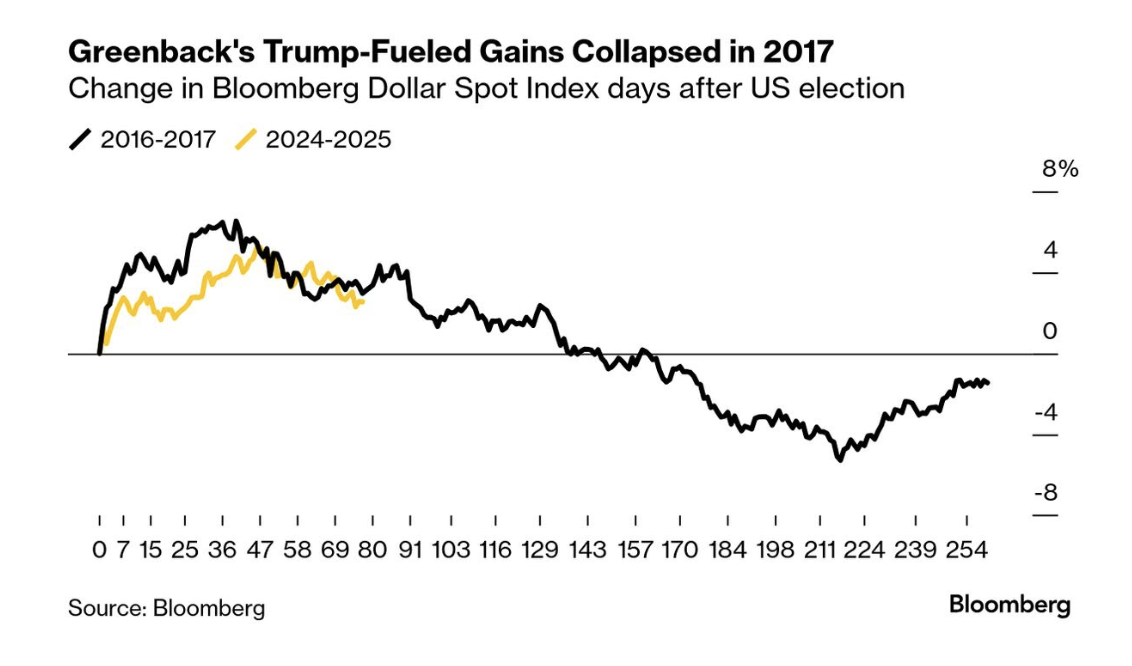

Trump = Weaker Dollar?: In 2017, trade policy and global growth concerns led to a sharp decline. The Bloomberg Dollar Spot Index initially surged after Trump’s re-election but has since reversed, with Morgan Stanley expecting further weakness. The bank attributes the dollar’s decline to less severe-than-expected tariffs and shifting investor expectations on U.S. trade policy. As a result, Morgan Stanley recommends long positions in the euro, yen, and pound against the dollar, expecting moderate appreciation in these currencies.

Bond Market is not buying what the DOGE is selling: Elon Musk, leading Trump's Department of Government Efficiency (DOGE), has made aggressive budget cuts, including shutting down USAID, but bond markets remain skeptical about their impact on the deficit. Despite claims of $55 billion in savings, actual figures appear much lower, and legal challenges threaten further cuts. Investors worry that Trump's tax cuts and tariffs could offset any spending reductions, keeping inflation high and preventing long-term interest rates from falling. Bond markets demand tangible results, as history shows that rhetoric alone won’t lower yields or stabilize the national debt.

Global Macroeconomic News:

Jobless Claims: Initial job list claims jumped by over 22,000 from 220k up to 242k indicating the impact of US Labor cuts spearheaded by Trump have had a profound impact on the labor market this data point will serve into the next few FOMC meetings with inflation Cooling and the labor market cooling we are primed for a further rate cut in a continuation of the federal easing cycle

PCE + Core PCE: PCE dropped to 2.5% from 2.6% in December indicating easing in the inflationary environment in the US as well as Core PCE dropping to 2.6% from 2.9% showing that food and energy prices with increased instability have caused dramatic differences between these two inflationary gauges.

Sources: Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, New York Times, Bloomberg, Wall St Journal, Washington Post, US Department of the Treasury

Have a great week investing!

Sincerely,

Aremorph

Comments

Post a Comment