CTSH: When the Gold Rush Comes, Invest in Shovels

Cognizant Technology Solutions Corp (NASDAQ: CTSH) Stock Pitch

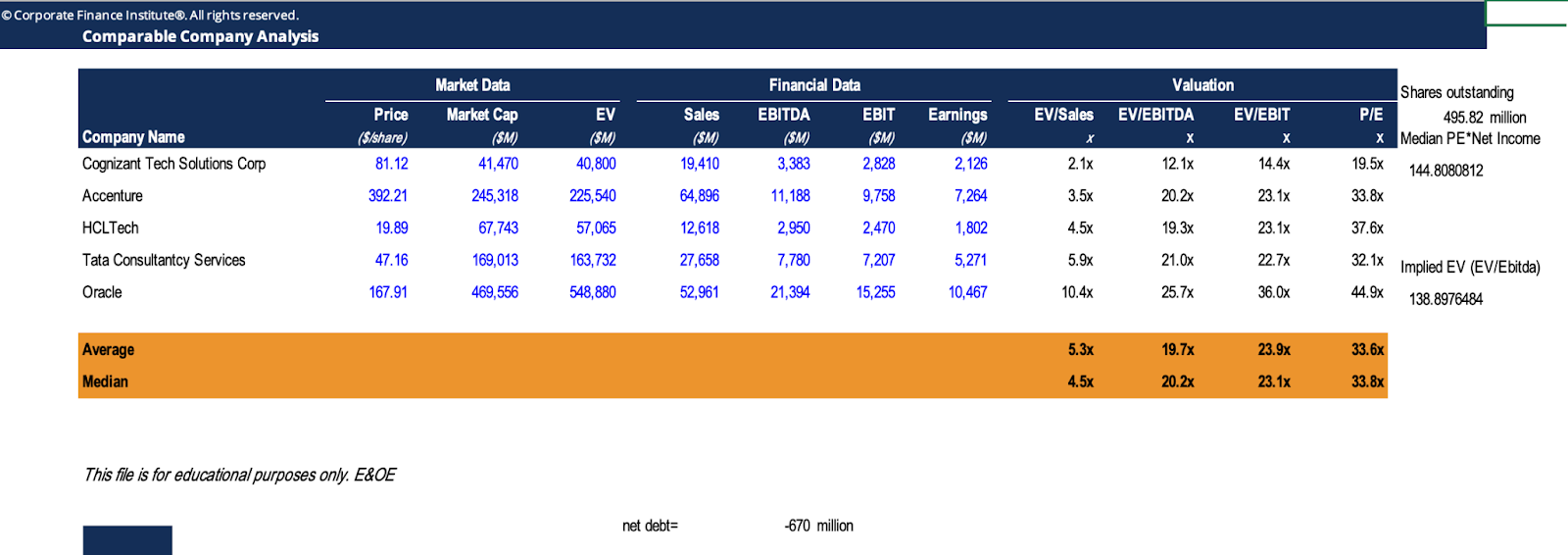

Investment Overview

Cognizant Technology Solutions Corp (CTSH) is a technology consulting firm focused on modernizing digital services across various industries. The company provides consulting in application development, system integration, cloud infrastructure, cybersecurity, business process automation, and AI-driven solutions.

Company Overview

Current Price: $90.70 (86.32 at time of research)

Target Price (1 Year): $108 (+20%)

Valuation: PE(20.13) * EPS(5.39)

Key Services: Application security, AI hubs, cloud transformation, infrastructure modernization

Key Partnerships: Adobe, Dell, Google Cloud, IBM, Palantir, Shopify, Workday, CrowdStrike

Geographic Reach: Operates in over 40 countries

Deal Activity: Closed 29 deals over $100M in 2024 (17 in 2023)

Investment Thesis

Attractive Valuation:

PE Ratio: 20.13 vs. Bloomberg ANR comp median of 25.65

EV/EBITDA: 11.35 vs. Bloomberg ANR comp median of 17.07

Acquisition Strategy: Cognizant has completed 6 acquisitions in the last 2 years, strengthening its technological capabilities and market presence.

Revenue Growth:

Healthcare revenue up 10%, led by TriZetto (processes ~66% of US healthcare claims)

North American revenue up 8.3% to $3.8B

Q4 revenue jumped by 450 bps YoY, largely driven by Belcan and Thirdera acquisitions

Catalysts

Tariff & Interest Rate Impact:

Tariff implementation and a higher interest rate environment could strengthen the USD against INR (24% of Cognizant’s expense base is in rupees).

Stronger USD lowers operating expenses, improving margins.

Higher US interest rates attract foreign capital, strengthening the dollar.

Political Tailwinds:

Potential Trump re-election could bring deregulation in antitrust laws, increasing M&A deal flow.

Expected rollback of Biden’s Section 5 broadening of FTC oversight, leading to fewer restrictions on M&A.

Tax cuts and reduced legal barriers could allow Cognizant to further expand via acquisitions.

M&A Execution:

Recently acquired Belcan for $1.3B, a key supplier in aerospace, defense, automotive, and industrial markets.

Acquisition-driven revenue boost, as seen in Q4 2024’s 450 bps revenue increase.

Risks & Mitigation

Sector Dependency: Cognizant relies on tech, financial, healthcare, and product/resource sectors. Fee and contract-based revenue could be impacted by margin compression due to tariffs.

Mitigation: Diversifying through acquisitions (e.g., Palantir, Belcan) to broaden service offerings.

Foreign Currency Risk: 26.3% of revenue comes from international markets, and 24% of costs are INR-denominated.

Mitigation: Cognizant hedges FX exposure using forward and option contracts.

Alternative Strategy: A long INR hedge could counterbalance a weaker USD impact.

Conclusion

Long CTSH with a 12-month price target of $108. The combination of a favorable macro environment (tariffs, interest rates, deregulation), undervaluation relative to peers, strong M&A execution, and AI/cloud transformation tailwinds positions Cognizant for upside potential.

Appendix (For Follow-ups)

Key Metrics & KPIs

P/E: 20.13

P/B: 2.87

Revenue Growth: 8.3% in North America, 10% in Healthcare

Goodwill as % of Assets: 14.26% (higher than comp median of 1.44%)

Earnings Call Notes

Associate consulting ideas doubled to 240K, with 47K solutions implemented by clients.

AI deployment for internal and client operations (identified 200 AI use cases).

Renewed deal with McDonald's for finance system and human capital management.

Signed a deal with Toyota for GenAI integration in software development.

20 bps upward revision in 2025 operating margin expectations.

Comments

Post a Comment