2/3-7/25 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Week 2/3-7/25

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

What a week! Welcome to all new members and welcome back to our returning members! As we stride into February, earnings seasons continue to sprinkle volatility into the equities markets. Moreover, data releases like ADP and Unemployment data changed the sentiment regarding the future interest rate environment.

Global Weekly Movements

U.S. Equities

S&P 500 Index: 6,025.99 (0.94%)

Dow Jones Industrial Average: 44,303.40 (0.008%)

Russell 3000 Index: 3,451.45 (1.03%)

NASDAQ Composite: 19,523.40 (1.60%)

Big Movers of the Week

Tesla (TSLA): 361.62 (-10.62%)

Tesla missed earnings and revenue estimates, with sales in France dropping 60%, overall sales down 33%, and a 11.5% year-over-year decline in Chinese sales. Intensifying competition from Chinese EV manufacturers and weaker global demand are raising concerns about Tesla’s future growth.

FMC Corp (FMC): 34.54 (-38.08%)

Net income for 2024 fell 74% to $342 million, and revenue declined 5% to $4.25 billion. In Q4, the company swung to a net loss of $16 million, despite a 7% increase in quarterly revenues to $1.22 billion. FMC's outlook for 2025 remains cautious, attributed to lower inventory levels and foreign exchange challenges.

Google (GOOGL): 187.14 (-8.98%)

Alphabet's fourth-quarter results disappointed, with its earnings falling short of expectations. Google’s core advertising business faced challenges, but despite these struggles, analysts pointed out that Google’s cloud business showed strong growth, and the company’s investments in AI and search products offer long-term potential.

Palantir (PLTR): 110.85 (34.48%)

Palantir Technologies saw a strong performance last week, hitting a record high of $116. This still marked a 34.38% increase from the previous week, driven by a 16% rise in net income for 2024, reaching $462 million, alongside a 29% revenue growth to $2.87 billion. U.S. revenues surged by 38%, with fourth-quarter figures showing a 10% increase in net income to $79 million and a 36% rise in revenues, including a 52% jump in U.S. revenues. This pushed Palantir’s market cap to $240 billion, surpassing companies like American Express, McDonald's, and Disney.

Expedia (EXPE): 202.37 (18.38%)

Net income for the fourth quarter soared 124% to $299 million, while revenues increased by 10% to $3.184 billion. For the full year, net income rose 55% to $1.234 billion, and revenues grew by 7% to $13.69 billion. Additionally, Expedia reinstated its quarterly cash dividend, set for distribution in March 2025.

Chinese Equities - Shanghai Composite (SHCOMP): 3,303.67 (2.51%)

Hong Kong Equities - Hang Seng Index (HSI): 21,133.54 (5.41%)

Japanese Equities- Nikkei 2225 (NI225): 38,787.02 (-0.37%)

European Equities

UK Index (UKX): 8,700.53 (0.31%)

German Index (DAX): 21,787.00 (2.28%)

Commodities

Gold Futures: 2,886.10 (2.65%)

Crude Oil Futures: 71.06 (-2.87%)

U.S. Monetary & Fiscal Policy:

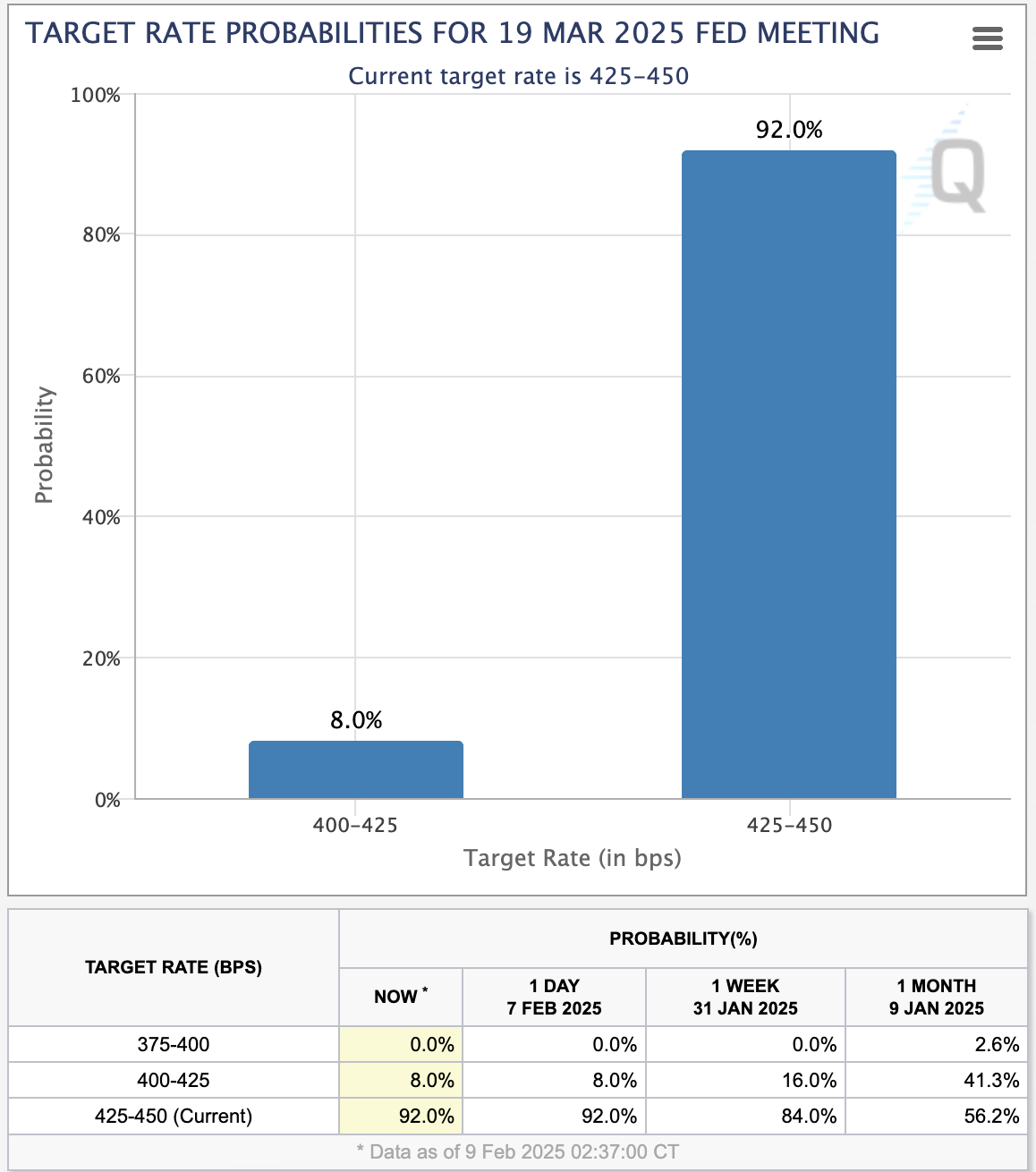

FOMC Rate Sentiment Changes: Market expectations for the March 19 FOMC meeting have shifted significantly, with a 92% probability of no rate cut and only an 8% chance of a 25 bps cut to 4.00–4.25%. A month ago, sentiment was more dovish, with a 3.6% chance of a 50 bps cut, 41.3% expecting a 25 bps cut, and 56.2% anticipating no change. The shift reflects continued labor market strength and persistent inflation, reducing the likelihood of imminent rate cuts. With inflation staying elevated and economic resilience intact, markets now expect the Fed to hold rates steady in the near term.

Chinese Retaliatory Tariffs: China retaliated against Donald Trump’s newly imposed 10% tariffs on Chinese goods by introducing levies of 10-15% on U.S. energy and agricultural equipment exports. Beijing launched an antitrust probe into Google and blacklisted PVH Corp. and Illumina Inc., signaling broader economic pressure. China also imposed export controls on tungsten and other critical metals, which could disrupt U.S. defense and technology sectors. Despite the response, Xi Jinping’s measures appeared calibrated to avoid major economic fallout, with markets reacting moderately. The restrained approach suggests room for negotiation, as Trump hinted at potential talks with Xi.

Global Macroeconomic News:

Jobless Claims & Unemployment: U.S. initial jobless claims rose by 11,000 to 219,000 in late January 2025, exceeding market expectations. The data suggests a slight softening in the labor market, though it remains historically resilient. Unemployment rate data shows a continued decrease in unemployment from 4.1% to 4.0%, with both inflation data (PCE) rising recently and the labor market increasing, there is a shift in market sentiment regarding future interest rate environment.

America in Gaza: Donald Trump proposed that the U.S. take control of Gaza, relocate its residents, and redevelop it into a luxury destination, sparking international backlash. Arab nations, including Saudi Arabia and Jordan, condemned the idea as forced displacement, while critics called it “ethnic cleansing by another name.” Trump suggested the U.S. could clear explosives and even deploy troops, though his plan lacked input from Palestinian officials. Netanyahu did not oppose the idea, and Trump proposed wealthy nations could fund the relocation of Palestinians.

ADP Employment: The U.S. economy added 143,000 jobs in January, with unemployment ticking down to 4%, indicating a cooling but still solid labor market. Job gains were lower than the expected 169,000, but upward revisions to November and December figures added 100,000 jobs. Hiring remains strong in sectors like healthcare, retail, and government, while mining and oil and gas extraction saw declines. Wages grew faster than expected, maintaining workers’ buying power, but potential policy shifts under the Trump administration—such as immigration restrictions and tariffs—could impact labor market trends. The Federal Reserve is likely to stay in a wait-and-see mode, focusing on inflation rather than immediate rate cuts.

Sources: Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, New York Times, Bloomberg, Wall St Journal

Have a great week investing!

Aremorph

Comments

Post a Comment