2/10-14/25 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Week 1/27-31/25

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

This week, inflationary data was released, the Eagles lit up the Chiefs, and retail sales and earning seasons continue to cause rallies across the markets. Check out below what impacted the markets and how they moved!

Global Weekly Movements

U.S. Equities

S&P 500 Index: 6,114.63 (1.13%)

Technology (XLK) led the bull charge, gaining at 3.07% in the past week, with supporters like SMCI, INTC, MU, and DELL. Many companies in the tech space, specifically with AI, proposed increased capital expenditures in AI advancement. This leaves investors optimistic about the integration of AI and modern technology. Communication (XLC) increased second most with 2.50%, led by TMobile (TMUS) after their partnership announcement with Starlink to provide 5G “as long as you can see the sky, you are connected.”

Dow Jones Industrial Average: 44,546.08 (0.34%)

Russell 3000 Index: 3,495.72 (0.97%)

NASDAQ Composite: 20,026.77 (1.82%)

Big Movers of the Week

Intel (INTC): 23.60 (23.56%)

Intel's shares were fueled by rumors and updates highlighting undervalued assets. The company’s lagging foundry business is drawing attention as U.S. policy pushes for domestic chip production. A potential joint venture with TSMC and support from Vice President JD Vance for U.S.-made AI chips boosted investor sentiment. While Intel's foundry business is struggling, it remains a key asset in the U.S.'s efforts to regain chip manufacturing dominance.

AirBnB (ABNB): 161.42 (19.59%)

Despite a slightly lower-than-expected revenue forecast for Q1 2025, Airbnb highlighted stable growth in its key "nights and experiences" metric. The company plans to invest up to $250 million in new ventures starting in May, without launching separate apps or brands. CEO Brian Chesky emphasized enhancing the Airbnb app to meet all needs, while expecting strong profitability with a 2025 EBITDA margin of at least 34.5%.

CVS (CVS): 65.83 (21.88%)

CVS beat earning expectations, driven by strong performance in its Aetna insurance unit. Analysts quickly raised their price targets, with Truist Securities bumping theirs to $76 per share.

Hims & Hers (HIMS): 60.47 (39.88%)

A Super Bowl ad promoting affordable GLP-1 weight-loss drugs sparked controversy for criticizing the U.S. healthcare system. The stock's climb to 100% year-to-date gain follows the Senate's approval of Robert F. Kennedy Jr. as Health Secretary, and optimism over the FDA's easing of drug shortages. Retail investor interest and concerns over supply for leading GLP-1 drugs from Eli Lilly and Novo Nordisk have fueled demand for alternative companies.

Super Micro Computer (SMCI): 47.91 (25.91%)

The company expects fiscal 2026 revenue to reach $40 billion, surpassing consensus by $10 billion, driven by DLC technology adoption in new data centers. For Q2 FY 2025, revenue is projected at $5.6–$5.7 billion, up 54% year-over-year, while net income per share remains flat.

Chinese Equities - Shanghai Composite (SHCOMP): 3,346.72 (1.17%)

Hong Kong Equities - Hang Seng Index (HSI): 22,620.33 (6.58%)

Japanese Equities- Nikkei 2225 (NI225): 39,149.43 (0.62%)

European Equities

UK Index (UKX): 8,732.46 (0.37%)

German Index (DAX): 22,513.42 (3.13%)

Commodities

Gold Futures: 2,893.70 (-0.35%)

Crude Oil Futures: 70.56 (-0.93%)

U.S. Monetary & Fiscal Policy:

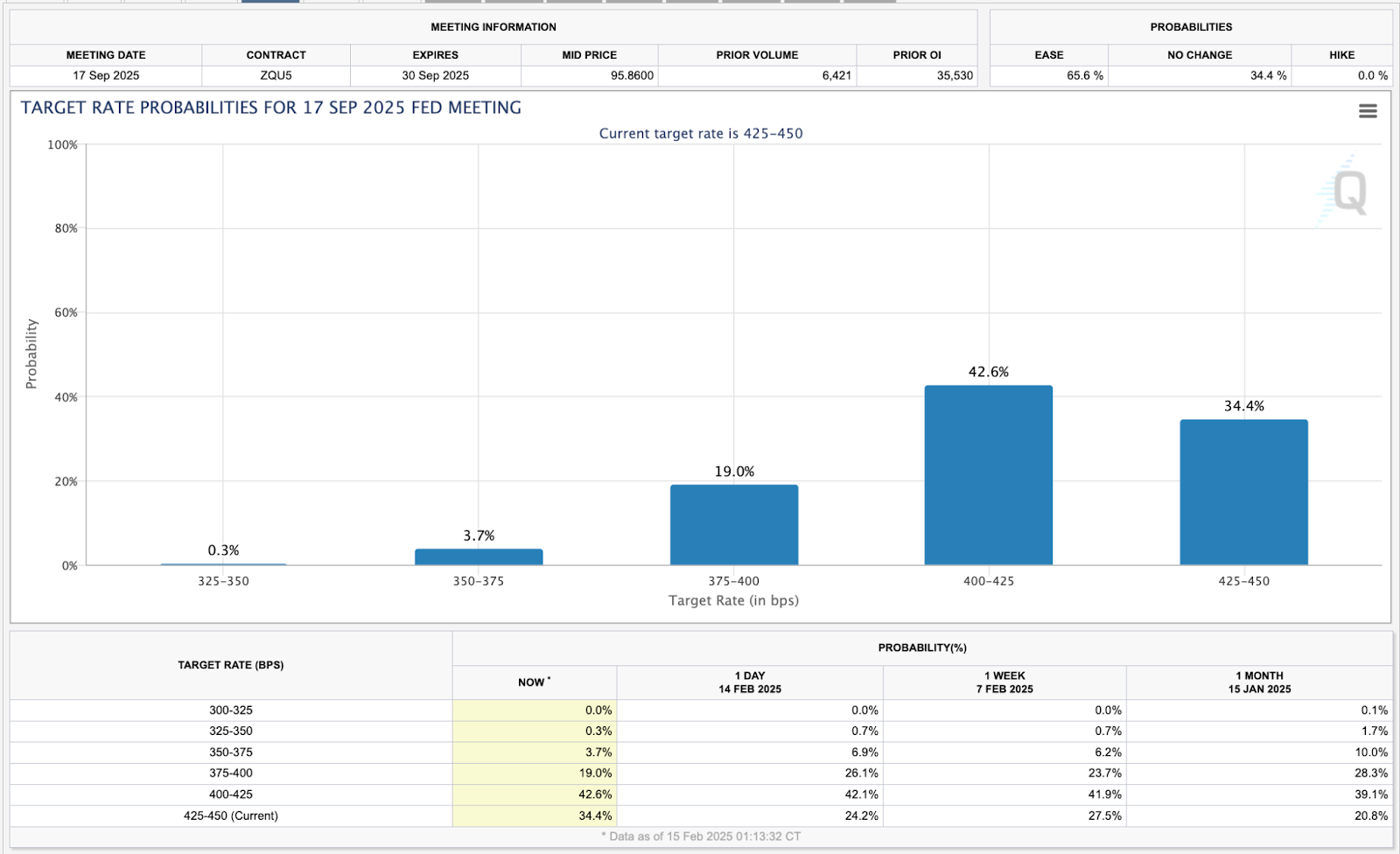

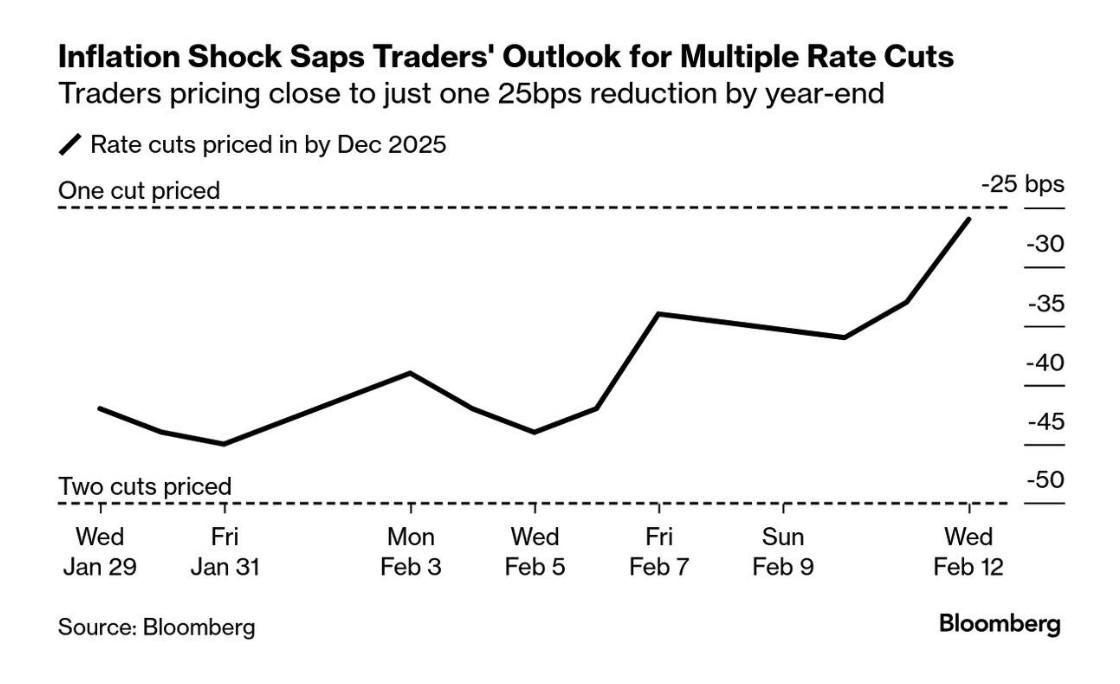

Sep 17th 2025 FOMC Meeting Futures: Expectations for the September 17, 2025, FOMC meeting have shifted notably. Futures now show a 34.4% chance of no cut, up from 20.8% last month, as inflation and labor data remain strong. The probability of a 50 bps cut has dropped to 19% from 38.3%, signaling reduced confidence in aggressive easing. With CPI running hotter than expected and the job market holding firm, the Fed may keep rates elevated longer. Markets are adjusting to the reality that the easing cycle is slowing.

Treasury Yields: The long end of the yield curve is down 25 bps, indicating an increase of demand for longer term treasuries. This could be a reaction to prospective weakening economic data if tariffs begin to force American citizens to pay tolls. With higher overall costs, discretionary spending could decrease, harming corporate earnings, and ultimately economic growth, contrary to how tariffs are typically supposed to bolster the economic strength of America by increasing their production and value of the USD.

Global Macroeconomic News:

CPI + Core CPI : The January 2025 CPI report showed increasing inflation, with headline CPI rising 0.5% MoM and core CPI increasing 0.4% MoM, bringing YoY inflation to 3.0% and 3.3%, respectively. Energy and food prices surged, with gasoline up 1.8% MoM and egg prices spiking 15.2% MoM due to the ongoing Avian flu. Core services inflation remained firm, driven by a 0.4% MoM increase in shelter costs, which contributed nearly 30% of the headline CPI rise.

Initial Jobless Claims: U.S. initial jobless claims fell by 7,000 to 213,000, while continuing claims dropped to 1.85 million, both beating expectations. The data underscores labor market resilience, reinforcing the Fed’s stance that rate cuts aren’t urgent. With declines in key states like Pennsylvania and New York, employment remains strong despite economic uncertainties.

US Retail Sales: Retail sales fell 0.9% in January, marking the biggest decline in a year, as extreme cold weather and post-holiday cutbacks dampened consumer spending. Auto sales and other discretionary purchases saw notable weakness, particularly in the South, which experienced its coldest January since 1988. While some analysts expected preemptive buying ahead of Trump’s proposed tariffs, the data showed no such rush. December sales were revised higher, suggesting some front-loaded holiday demand.

Chinese Gold: China has launched a pilot program allowing insurers to allocate up to 1% of their assets to gold, potentially unlocking $27.4 billion in new demand. This move comes as gold prices hit record highs, fueled by Federal Reserve rate cut expectations, central bank purchases, and geopolitical uncertainty. The policy shift reflects China’s search for alternative investment options amid a property market downturn and slowing economic growth. While insurer demand may build gradually, it marks a significant step in integrating gold into institutional portfolios. With limited mid-to-long-term assets offering stable yields, gold’s role in China’s financial landscape could expand further.

Sources: Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, New York Times, Bloomberg, Wall St Journal, Washington Post, US Department of the Treasury

Have a great week investing!

Sincerely,

Aremorph

Comments

Post a Comment