1/20-24/25 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Week 1/20-24/25

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

Earnings season is upon us again! Among other events such as jobless claims and consumer sentiment. Lets dive into some earnings reports and global events that shaped the market! Moreover, Trump is back in office!

Global Weekly Movements

U.S. Equities

S&P 500 Index: 6,101.24 (1.77%)

All sectors of the SPX positive on the week except for energy at (-2.82%). Utilities and Communication services led the charge, gaining 4.31% and 3.10% respectively. Utilities say a boost under Trump’s Stargate plans. Mentioned below, Netflix led the charge in XLC. Overall, we are seeing the initial impact of Trump’s inauguration taking shape.

Dow Jones Industrial Average: 44,424.25 (2.57%)

Russell 3000 Index: 3,491.48 (1.89%)

NASDAQ Composite: 19,954.30 (1.52%)

Big Movers of the Week

Netflix (NFLX): 977.59 (13.89%)

Netflix closed with an all time high after citing strong fourth quarter earnings, with a 18.9 million subscriber gain, the largest in its history. Wall st analysts raised the spot price target to $1,250. Netflix announced a $15 B stock buyback and increased revenue outlook by 1B from 43.5B to 44.5B. Netflix’s new direction in entertainment with events like NFL, Boxing, and exclusive shows are driving revenue and membership up. Couple this with decreasing core CPI, and potential continued Fed easing, I expect discretionary spending to increase.

EA stock (EA): 116.56 (-18.76%)

EA stock tanked as revision to 2025 guidance took place, decreasing revenue forecasts. Most recently, EA games has lost its partnership with FIFA for soccer video games which harmed their market dominance.

Charles Schwab (SCHW): 81.83 (7.02%)

Under the new CEO Rick Wuster, Schwab Q4 earnings boasted a 20% increase in revenue and nearly an 80% increase in net revenue. These impressive figures rallied investors, but despite these figures, analysts are concerned at why retail NNA growth is slow at 3.5% despite strong performance across the firm. Wurster reassured investors that the priority at the moment was gaining trust of integrated TD Ameritrade clients.

Moderna (MRNA): 41.41 (22.48%)

Despite a 90% downturn in the stock during the past year, investors rallied behind Moderna as they secured a contract for COVID-19 vaccines with the EU. Moreover, after the inauguration of Trump, discussion of Project Stargate and the integration of AI into vaccine development presented a positive outlook for the company's potential.

Chinese Equities - Shanghai Composite (SHCOMP): 3,252.63 (-0.11%)

Hong Kong Equities - Hang Seng Index (HSI): 20,066.19 (1.32%)

Japanese Equities- Nikkei 2225 (NI225): 39,931.98 (3.26%)

European Equities

UK Index (UKX): 8,502.35 (-0.03%)

German Index (DAX): 21,394.93 (2.36%)

Commodities

Gold Futures: 2,777.4 (1.17%)

Crude Oil Futures: 74.6 (-4.9%)

U.S. Monetary & Fiscal Policy:

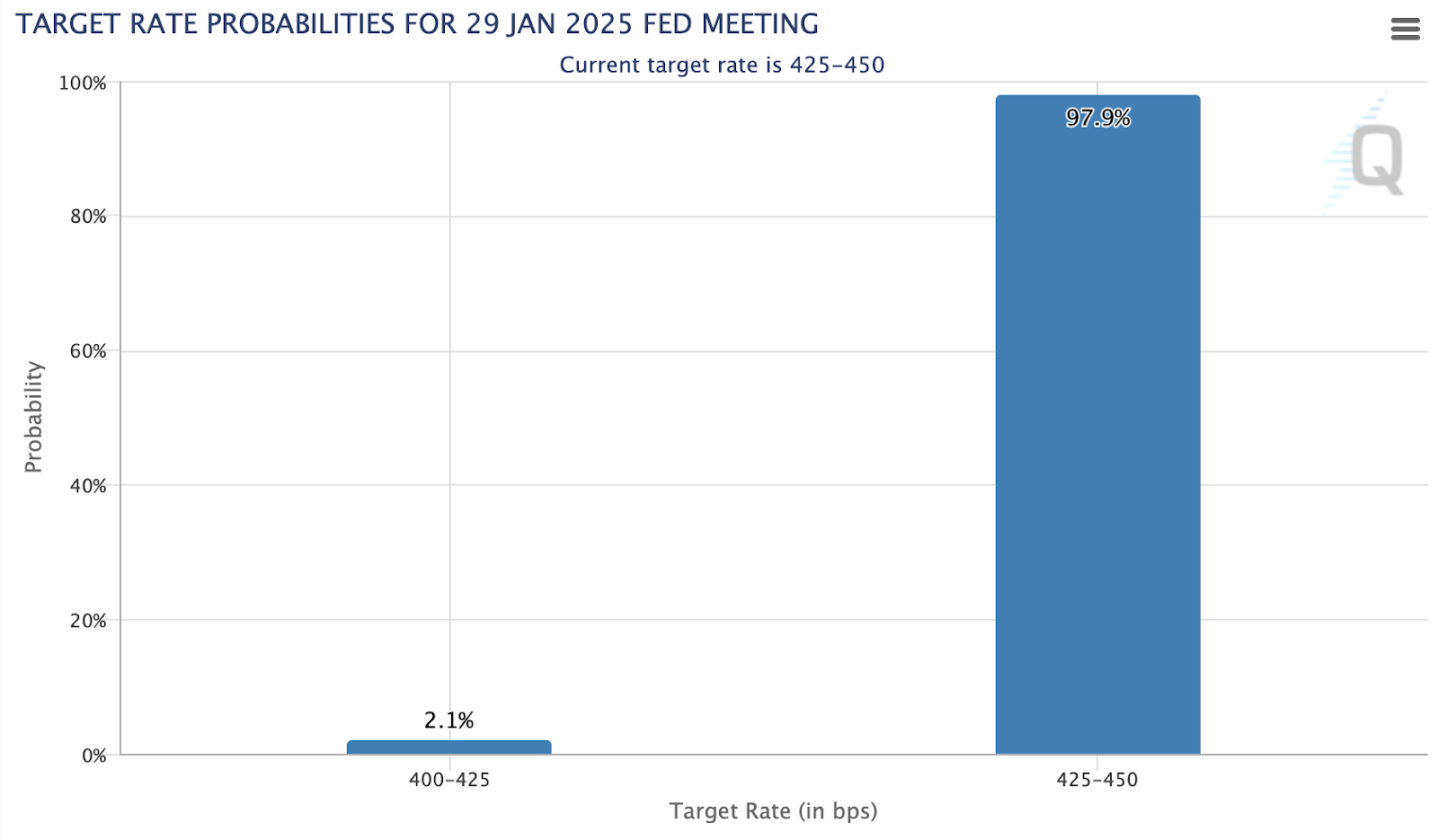

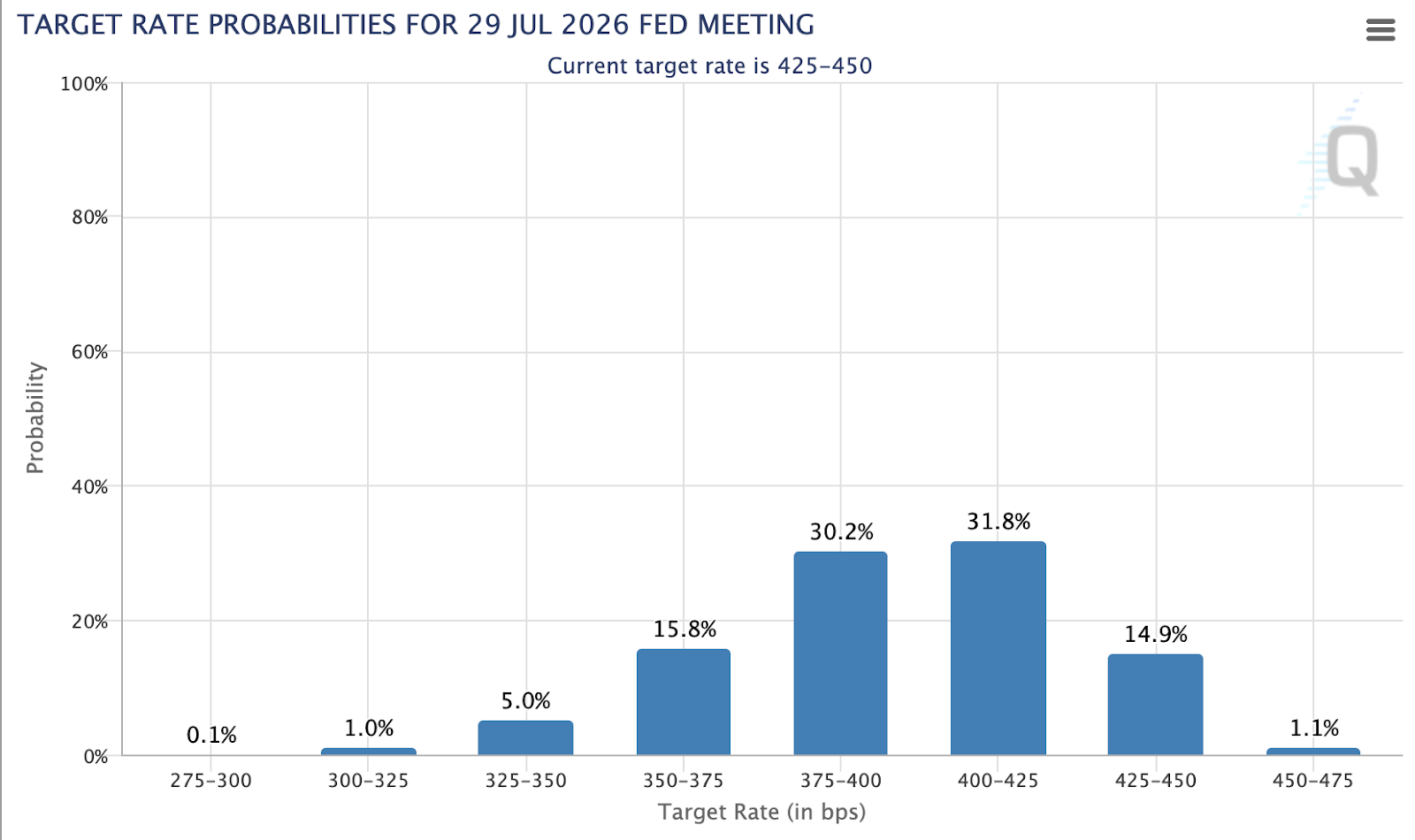

FOMC Meeting on Jan 29th:

The market is pricing in no change to the Fed Funds Rate and insistent that the Fed will not cut until at the earliest, July 29th, 2026. With this overall expectation of an easing interest rate environment, equities will seem more attractive, impacting investment volume. Given Trump’s recent discussion of considering harsh tariffs, it seems unlikely that harsh inflationary pressures will be implemented, leading to increased confidence in the continuation of the Fed easing cycle. The 1.5 year projection of interest rates still falls around a 25-50 basis point cut from now.

Equity Risk Premium Q1 2025:

Currently, many calculations of the equity risk premium of the 10 year market returns compared to 10 year treasuries (risk free) indicate a negative value. With a negative premium, investors are essentially paying to buy into equities and receive a projected return lower than that of treasuries. Analysing the short end of the yield curve and similar equity future estimates, we can see that the 1 year treasury yields at 4.184% are higher than the forward projection of the SPX over 1 year.

Global Macroeconomic News:

Jobless Claims: Jobless claims continued to rise this week by 6,000. The fires in LA are having some extended impacts on the labor market. This continued slowing on the labor market can be a positive indicator for continued Fed easing, as investors are keen to see if the near future interest rate environment will stagnate or decrease.

Inauguration: Trump marked as the second president to return to office without a consecutive election process. This time around, many large tech companies are excited to voice open support of his intentions, with mega cap CEO’s like: Tim Cook, Mark Zuckerberg, Elon Musk, Jeff Bezos, and Shou Chew. This collaboration between policy and industry can have an exponentially positive impact on tech equities and overall deal flow. Trump immediately prescribed 78 executive orders, pardoned over 1,500 rioters, and ordered the US to withdraw from the WHO. This uptick in volatile actions can be expected to move markets, many say bullishly. Trump touted 25% tariffs on Canada and Mexico by Feb 1, while reserving tariffs on China for negotiating leverage.

Potentially Impacted Securities: AAPL, META, TSLA, AMZA, MSFT

BOJ Rate Hike: The Bank of Japan (BOJ) raised its key policy rate to 0.5%, the highest level since 2008, citing stronger inflation expectations and setting the stage for potential future hikes. The yen strengthened and impacted Japanese stocks, with 10-year bond yields rising. Governor Kazuo Ueda emphasized flexibility in future rate decisions, tying them to economic and price trends, while maintaining no fixed timeline for additional hikes. Inflation projections were increased, signaling confidence in sustained price growth, though concerns over exchange rates and import prices remain.

Potentially Impacted Securities: USD/JPY

Stargate AI vs Elon: Elon Musk’s involvement in Trump’s administration as both a government efficiency adviser and an ally highlights potential conflicts of interest, especially amid his criticism of Trump’s $500 billion Stargate AI project. Musk, who has competing AI ambitions and a legal feud with OpenAI’s Sam Altman, has publicly called the project underfunded and its founders untrustworthy. Despite Musk’s outbursts, Trump appears unfazed, viewing their business rivalry as a manageable issue and valuing Musk’s strengths in his administration. The situation underscores the complexities of Musk’s dual role as a private-sector leader and government influencer. With two competing parties, fundamental stocks to AI like energy and data centers could perform handsomely regardless of the successor.

Sources: Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, New York Times, Bloomberg, Wall St Journal

Have a great week investing!

Sincerely,

Aremorph

Comments

Post a Comment