11/25-11/29/24 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Week 11/25-11/29/24

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

Happy Thanksgiving week! This week saw many fluctuations with macroeconomic indicators being released such as: new home sales, consumer confidence, jobless claims. This week was also special due to the stock market closing on Thursday, and early at 1pm on Friday.

Global Weekly Movements

U.S. Equities

S&P 500 Index: 6,032.38 (1.48%)

All sectors of the SPX were up this week, except for Energy (XLE) which saw increased geopolitical tensions impact equities prices. Healthcare (XLV) and Real Estate (XLRE) led the charge at (2.25%) and (2.06%) respectively, with Consumer Discretionary (XLY) close behind at (1.93%). These changes reflect the rebound from the RFK announcement as well as promising macroeconomic indicators.

Dow Jones Industrial Average: 44,910.65 (2.37%)

NASDAQ Composite: 19,218.17 (1.33%)

Big Movers of the Week

Ulta Beauty (ULTA): 386.64 (14.13%)

Ulta Beauty saw a surge this week after industry peer Bath & Body Works reported strong earnings as well as robust guidance, signaling sustained demand for personal care products.

Moderna (MRNA): 43.06 (12.58%)

Despite stock plunged after Robert F. Kennedy’s nomination, Moderna has seen some price recovery through positive phase 3 next-gen COVID-19 vaccines, Canadian approval of their RSV vaccine, as well as advancement with Merck in phase 3 for lung cancer combination treatment.

Autodesk (ADSK): 291.9 (-7.45%)

Autodesk, a leading engineering software platform, fell short on guidance after earnings after the announcement of a new CFO. This pullback is also a victim of swelling unsustainable expectations after the stock jumped from $200 to $317 in just 4 months.

Chegg (CHGG): 2.11 (18.54%)

After the release of GenAI in 2021, “homework helper” Chegg saw a steady decline until today. (-98.14) Falling into almost penny stock-status, speculative moves of ¢33 cause a 20% shift in the weekly performance.

Chinese Equities - Shanghai Composite (SHCOMP): 3,326.46 (1.57%)

Hong Kong Equities - Hang Seng Index (HSI): 19,423.61 (0.60%)

Japanese Equities- Nikkei 2225 (NI225): 38,208.03 (-1.22%)

European Equities

UK Index (UKX): 8,287.30 (0.31%)

German Index (DAX): 19,626.45 (0.84%)

Commodities

Gold Futures: 2,673.90 (-1.51%)

Crude Oil Futures: 68.15 (-2.98%)

U.S. Monetary & Fiscal Policy:

CME Fedwatch: In just one week, market sentiment has shifted significantly favoring the likelihood of a 25 bps Federal Reserve rate cut. As of November 22, the odds for a rate cut stood at 52.5%, with 47.5% predicting no change. By November 29, expectations for a cut surged to 66%, with just 34% anticipating rates to hold steady. This reflects the market sentiment based on economic data and market conditions, especially given the Fed is “data dependent,” PCE is steadily increasing and jobless claims remain superb.

Treasury Yields: This week, Treasury yields dropped, reflecting shifting market sentiment. Lower yields often indicate expectations of decreasing inflation and interest rates, moreover, cheaper borrowing can help boost economic activity, boosting economic activity and corporate earnings. This change also makes equities more attractive compared to fixed income, as we mentioned last week through the equity risk premium.

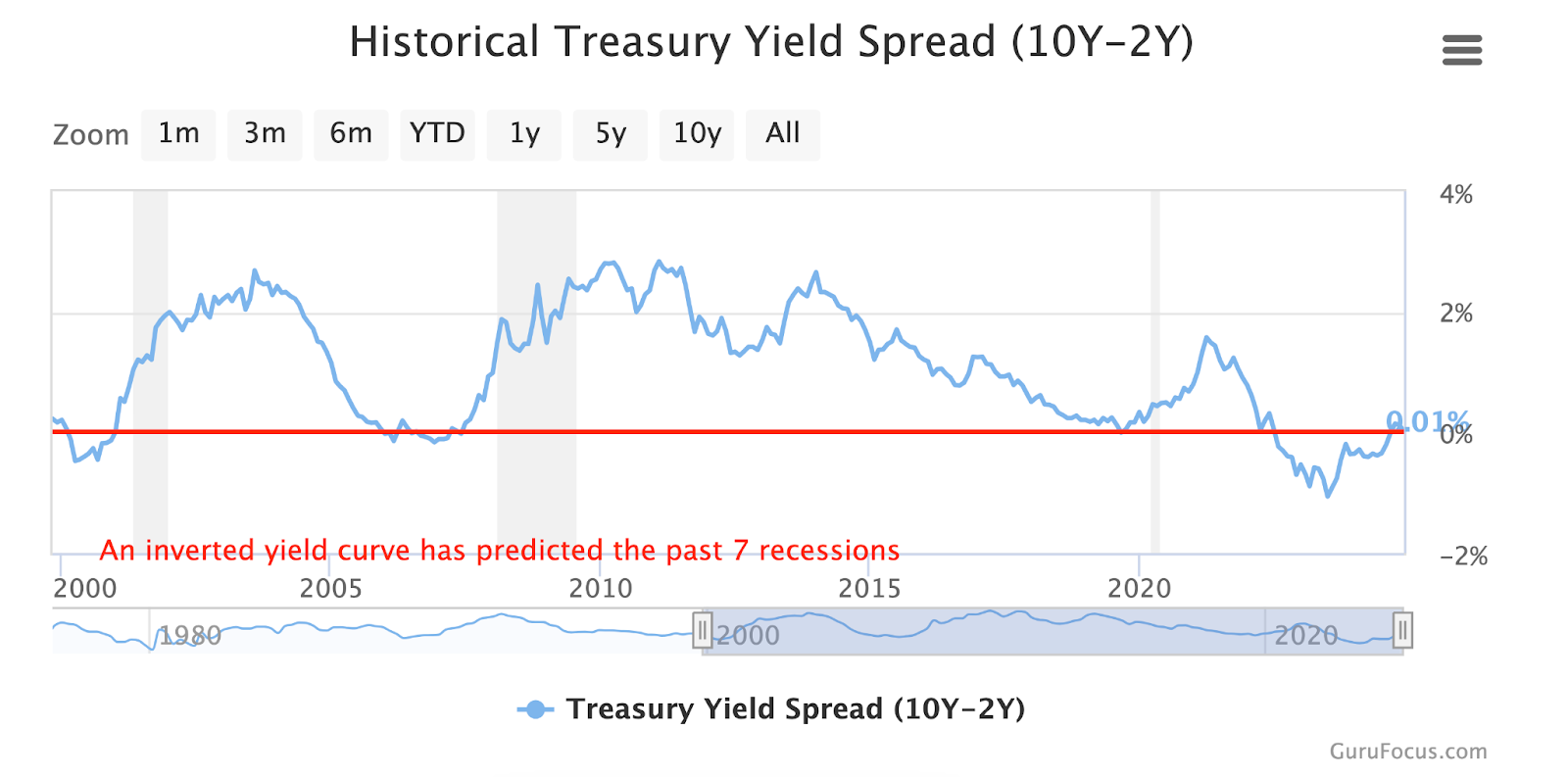

Historical Treasury Yield Spread: Dancing with Recession: The 10-year and 2-year treasury yield spread has been negative for 2 years, just cresting to .015 in November 2024, marking the longest and deepest inversion since the Great Recession in 1980. Unlike in 08’ and 20’, when the spread briefly rested at 0, sustained negative territory heightened fears of recession. Now, as the economy throws signs of revival and soft/no landing, the spread has returned to positive.

Dollar Under Trump: With a rally of the USD occurring recently due to strong economic data and favorable interest rate differentials, Trump could push this charge if new tariff policies are enacted. Economics at Aviva Investors indicate that tariffs may heighten inflation and widen the US-Global rate gap, enhancing the dollar’s “safe-haven” appeal. This is because higher inflation could prompt the Federal Reserve to maintain or raise interest rates, making U.S. assets more attractive to global investors seeking stability and better returns during times of economic uncertainty. For traders, this creates opportunities for long USD positions, especially against weaker currencies such as the CNY, JPY, or recently, the EUR.

Global Macroeconomic News:

PCE: The PCE price index rose by 0.2% in October, contributing to a 2.3% year-over-year increase. This reflects steady inflation, with the PCE continuing to track below the Federal Reserve's target of 2%. The modest rise in PCE suggests that inflationary pressures are stabilizing, which may influence the Fed's decision on future interest rate cuts.

New Home Sales: October's new home sales came in at 610k, significantly below the predicted 725k. This marked a slowdown in the housing market, potentially driven by higher mortgage rates and affordability concerns. The weaker-than-expected sales data could indicate challenges in the housing market, potentially impacting broader economic growth and consumer sentiment. This can also be a reflection of high interest rates, incentivizing people from purchasing homes and locking in high rates.

Consumer Confidence: CCI came in at 111.7 for November, slightly above the forecasted 111. With 1985 serving as the baseline year (set at 100), a reading of 111.7 indicates that consumer sentiment remains above the historical average. Despite concerns about inflation and interest rates, this level of confidence suggests households are resilient, which supports ongoing consumption and economic activity, given that 68% of the US GDP is PCE.

Potentially Impacted Securities: XLY, AMZN, MCD, SBUX

Jobless Claims: Initial jobless claims for the week were 213k, in line with expectations and slightly lower than the previous week's 215k. This stable job market data signals that layoffs remain low, supporting the broader economic outlook. Continued low jobless claims suggest resilience in the labor market despite other macroeconomic headwinds.

US $680 Million Arms Sale to Israel: The Biden administration has notified Congress of a major new weapons transfer to Israel, valued at $680 million. The decision to move forward with the sale came in late October and marks the latest sign of continued U.S. support for Israel's defense, amid ongoing conflict in Gaza and a recently agreed cease-fire in Lebanon.

Potentially Impacted Securities: Crude, XLI, BA

Sources: Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, GuruFocus, New York Times

Have a great week investing!

Sincerely, Aremorph

Wow! You really break down some finance concepts well, looking forward to next weeks!

ReplyDelete