11/18-11/22/24 Weekly Market Recap - Movers, Macro, Monetary, and Fiscal

Weekly Market Summary by Aremorph

Summary - Movers, Macro, Monetary, and Fiscal

With another week full of market movements and surprises from earnings reports, the equities market saw a lot of movement! With big companies like Walmart, Target and Nvidia shocking investors, jobless claims reverberating a stronger-than-expected market, and heightening geopolitical tensions in Europe, there are so many things to cover! Take a look below for the movements of the week!

Global Weekly Movements

U.S. Equities

S&P 500 Index: 5,969.34 (1.62%)

Dow Jones Industrial Average: 44,296.51 (1.99%)

NASDAQ Composite: 19,003.65 (1.53%)

Big Movers of the Week

Super Micro Computer Inc (SMCI): 33.15 (65.42%).

The troubled tech stock soared as the company announced new auditor contracts as part of its efforts to avoid delisting from NASDAQ.

Netflix (NFLX): 897.79 (10.18%).

Thanks to the amount of increased subscribers, mostly from the Jake Paul vs. Mike Tyson match, stock of the streaming services company soared and received price target hikes.

Ulta Beauty (ULTA): 338.38 (-7.34%).

Target (TGT): 125.01 (-18.29%) vs Walmart (WMT): 90.44 (6.42%).

This week highlighted a stark contrast between Target (TGT) and Walmart (WMT), as their performances diverged sharply. Target faced significant challenges, with disappointing third-quarter results marked by missed earnings and revenue estimates and reduced full-year guidance. Meanwhile, Walmart thrived, with strong earnings fueled by its focus on groceries, essentials, and e-commerce thanks to their ability to attract budget-conscious and higher-income shoppers, combined with effective cost management, underscores its resilience and strategic edge in the current economic climate.

Tesla (TSLA): 352.56 (3.47%)

Chinese Equities - Shanghai Composite (SHCOMP): 3,267.19 (-2.32%)

Hong Kong Equities - Hang Seng Index (HSIK): 19,229.97 (1.89)

Japanese Equities- Nikkei 2225 (NI225): 38,283.85 (.06%)

European Equities

UK Index (UKX): 8,262.08 (2.46%)

German Index (DAX): 19,322.59 (.38%)

Commodities

Gold Futures: 2,718.20 (4.68%)

Crude Oil Futures: 71.18 (1.54%)

U.S. Monetary & Fiscal Policy:

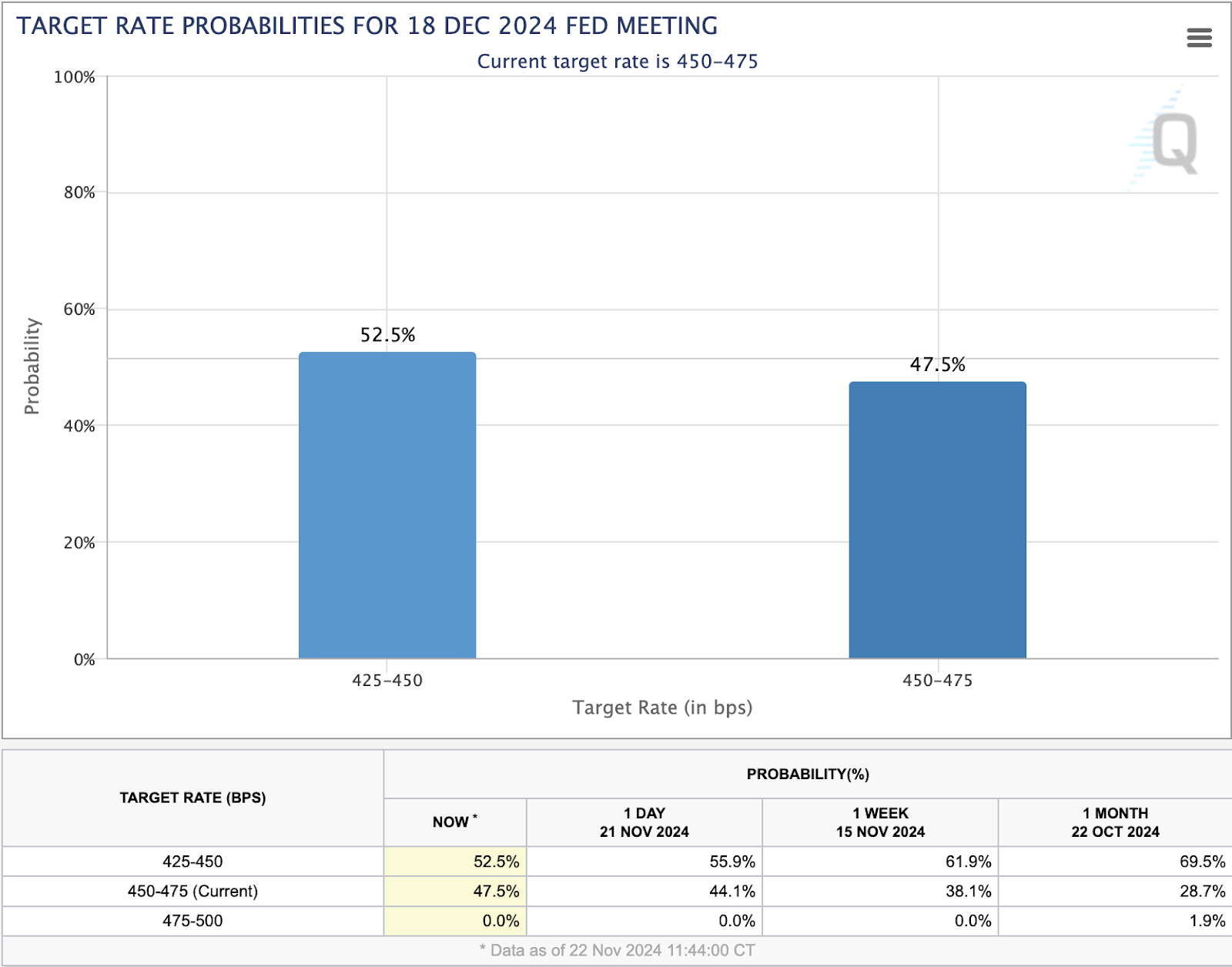

CME Fedwatch: Over the past week, there has been a noticeable shift in market expectations regarding a potential rate cut by the Fed. On November 14, 2024, the probability of the Fed keeping rates between 425-450 basis points stood at 72.2%, with a 27.8% chance of no rate cut. However, by November 22, 2024, these expectations had shifted significantly, with the probability of maintaining rates in the 425-450 bps range dropping to 53.5%, while the likelihood of no rate cut rose to 47.5%. This change reflects growing uncertainty in the market sentiment, as investors adjust their outlook on the Fed's monetary policy, emphasizing Jerome Powell's quote of the market not giving any signs to cut rates.

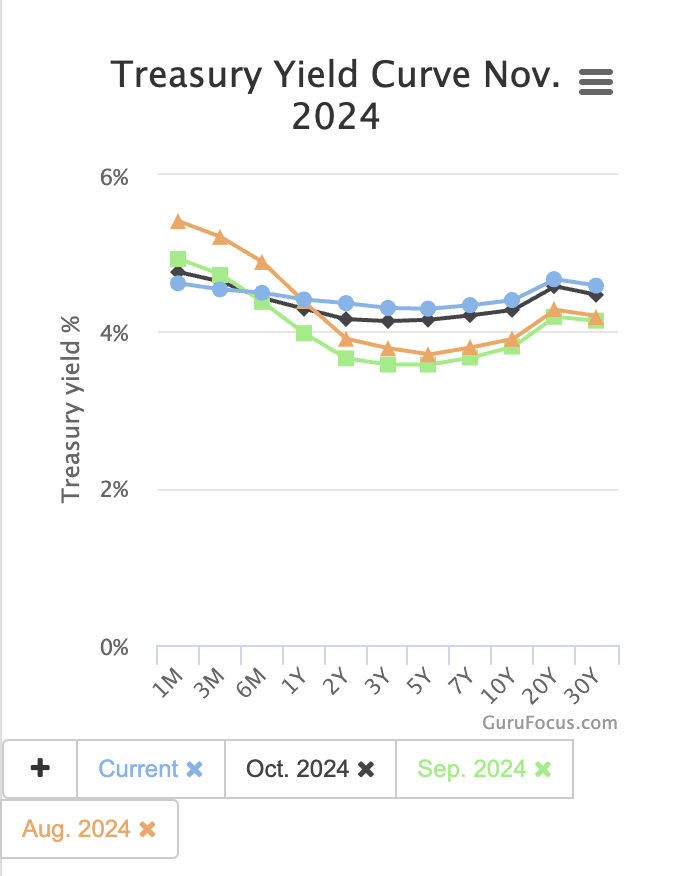

Treasury Yields: In August 2024, the Treasury yield curve was inverted, with the 1-month yield (5.41%) surpassing the 30-year yield (4.20%), signaling recession fears and expectations of economic slowdown. However, by November, the curve began to flatten, with the 1-month yield (4.617%) now only slightly higher than the 30-year yield (4.588%). This flattening suggests that while inflation concerns persist, investor sentiment has shifted towards a more stable economic outlook, with expectations of slower growth rather than an imminent recession.

Trump Tariff and Immigration: Fading "Trump stock euphoria" reflects growing concerns that his policies could introduce inflationary pressures and labor shortages. If Trump reinstates tariffs or escalates trade tensions, it could raise the cost of imports, fueling inflation and putting pressure on corporate margins and consumer spending. Additionally, increased deportations could tighten the labor supply, especially in sectors like construction and hospitality, leading to understaffing and higher wages. These factors may heighten operational costs, slow economic growth, and create more market volatility, dampening investor confidence.

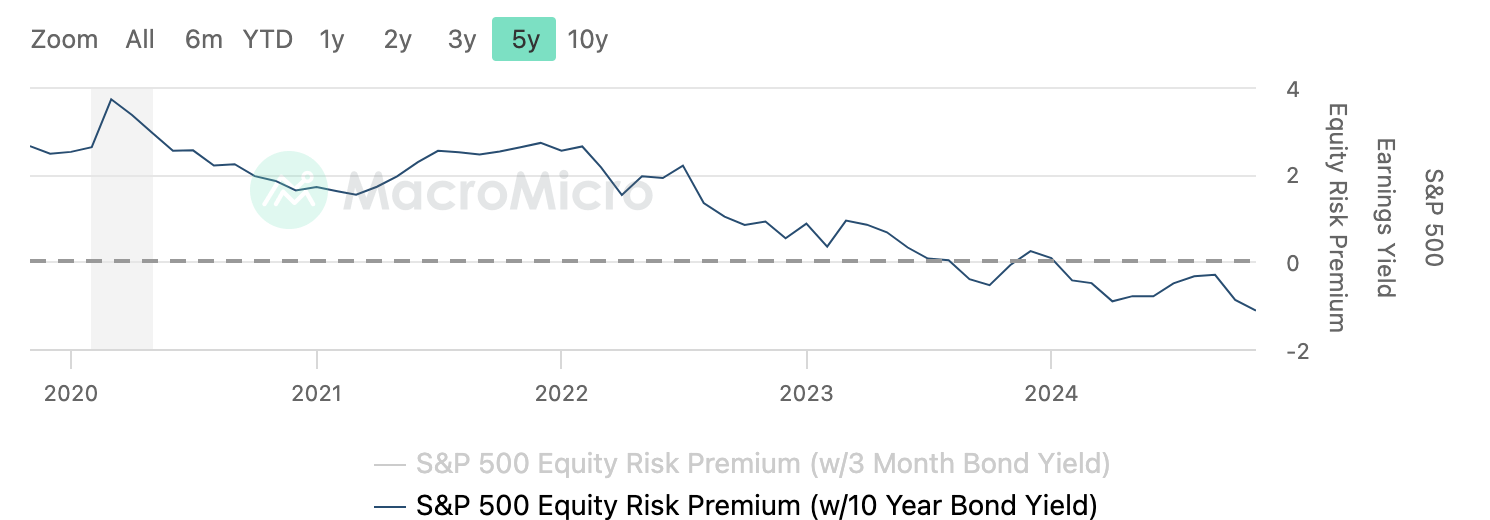

SPX Equity Risk Premium: The S&P 500's equity risk premium (ERP) is sitting below zero, signaling that investors are expecting lower returns from stocks compared to risk-free Treasury bonds. This unusual shift suggests that the stock market may be overvalued, or investors are showing heightened risk aversion. When the ERP is negative, it often points to potential market corrections ahead, as equities become less appealing than safer bonds despite their lower yields. This could be a warning sign for investors to tread carefully in the current market, especially after the aforementioned Trump euphoria.

Global Macroeconomic News:

Economic Output: U.S. economic output hit its highest level since April 2022, with the S&P Global flash PMI for November rising to 55.3, reflecting strong business activity, particularly in services. Optimism fueled by expectations of lower interest rates and a more pro-business environment under the incoming Trump administration has shifted investor focus from tech stocks to blue chips linked to economic growth. As a result, the Dow Jones Industrial Average rose, while the tech-heavy NASDAQ saw declines.

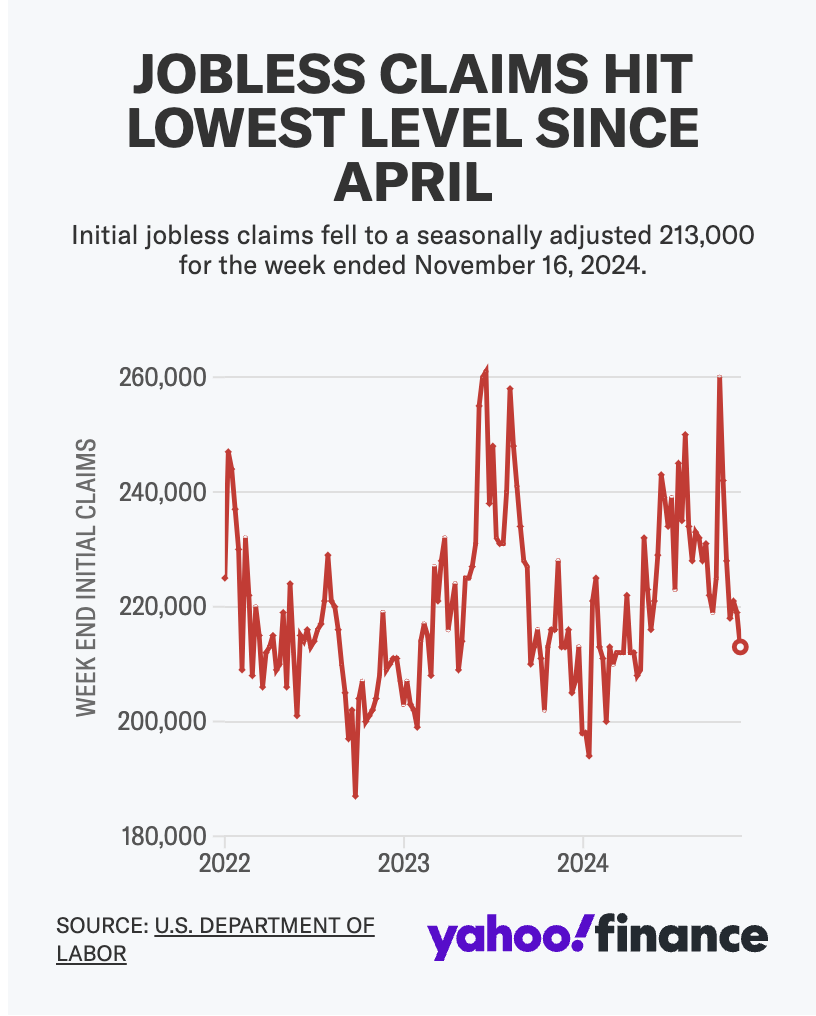

Jobless Claims: Jobless claims fell to a seven-month low of 213,000 for the week ending November 16, coming in better than expected. The trend points to a resilient labor market. Continuing claims did tick up to 1.9 million—the highest since 2021—but overall layoffs remain low, and the unemployment rate is steady at 4.1%. The labor market is looking healthier, which has led the Fed to take a more cautious approach on rate cuts.

Russia & Ukraine: Ukraine’s first use of U.S.-supplied ATACMS missiles on Russian soil marks a dramatic escalation in the war. The strike on a Russian ammo depot has prompted fierce reactions from Moscow, with Putin warning of potential nuclear retaliation. The move comes after thousands of North Korean troops joined Russia’s war effort, prompting fears of further escalation. Expect heightened market volatility, especially in equities as geopolitical tensions rise. Nuclear threats from Putin caused equities to fall back on Tuesday and Wednesday. Gold saw a bump as investors hedge against uncertainty, while the ruble and Eastern European currencies may feel the pressure.

Potentially Impacted Securities: LMT, RTX, BP, XOM, Gold

ICC issues arrest warrant for Israel’s Netanyahu: The International Criminal Court (ICC) has issued arrest warrants for Israeli Prime Minister Benjamin Netanyahu and former Defense Minister Yoav Gallant, accusing them of war crimes in Gaza, including murder, persecution, using starvation as a weapon, and harming children. This unprecedented move could make international travel tricky for the two leaders, as they risk arrest in any of the 124 ICC member countries. The warrants come as Israel faces growing global isolation over its handling of the Gaza conflict, and could lead to more legal challenges or shunning of Israeli officials. It's a serious hit to Israel’s diplomatic standing, and will likely have ripple effects across Europe and beyond.

Sources: Bloomberg Terminal, Google Finance, Market Watch, CME Fedwatch, Yahoo Finance, Reuters, GuruFocus, New York Times

Have a great week investing!

Sincerely,

Aremorph

Comments

Post a Comment